Harrison Willis

Harrison Willis

Introduction

Multifamily investments, particularly value-added strategies, have been of keen interest to real estate investors for years now. Successful execution of a multifamily investment offers excellent risk-adjusted returns when compared to other classes of real estate such as industrial, retail, and office. From a volatility standpoint, multifamily enjoys relatively stable long-term cash flows with less downside risk during periods of recession due to stable tenancy in most major markets. The stability during downturns is also supported by the fact that recessions tend to make renters out of owners, increasing demand for apartments.

Multifamily has enjoyed sustained rent growth over the last decade, driven in large part by the Millennial generation graduating from college and moving into the job market. Millennials are settling down and starting families later than previous generations, which has resulted in their tendency to rent for longer periods. The size of the Millennial generation, buttressed by their tendency to rent longer than previous generations, has driven demand for rental units and grown rents throughout the United States.

This growth in rents, coupled with the general stability of rental units, has led to an increased demand for multifamily properties by institutional investors, and subsequently led to the continued replacement of traditional mom and pop owners in the sector. This has been accentuated in the current market, as institutional investors are starved for yield from stable sources of cash flow due to low interest rates and other factors. Investors have been chasing yield and buying rental properties at low cap rates, making it difficult to find good deals in much of the United States. The pursuit of safe yields is especially true when it comes to class-A properties, and properties in core markets.

That said, there are still opportunities to find individual properties and deals outside of the class-A range. These opportunities are the key to one of the most exciting prospects in real estate: the value-added multifamily play. This occurs when an investor buys an underperforming asset, and then creates value by investing in the refurbishment of the structure or its operations. This can be done in a number of ways, but the main point is that this strategy allows the investor to increase rents and sell the property at a premium once the repositioning or refurbishment has been successfully completed.

This article delves into the different aspects of a value-added investment, detailing what to look for in a property, what to watch for during the investment period, and the checklist when it comes to creating value. As properties vary greatly from market to market, this article focuses on the nuts and bolts of making the investment, realizing a value-added strategy, and exiting the property. By the end of this brief, the reader should have a general understanding of what goes into a traditional value-added approach to a Class-B garden-style apartment multifamily investment.

The Top-Down

The first part of the value-added process is the acquisition strategy. The most important part of the strategy is to base the returns on conservative metrics by finding an undervalued property. The value that one gets in the beginning of a deal will set the transaction up for success, and give the investor a margin of safety.

Targeting value is much more important for an overall strategy than it is for a single deal, as a single deal is more dependent on market timing, and the dynamics of the local market of that investment. While the two might seem mutually exclusive, they are not. As Benjamin Graham famously said, “In the short run, the market is a voting machine, in the long run it is a weighing machine.” The same method can apply to a real estate strategy. In the short run, the variety of factors that affect a deal can mask a mistake in underwriting. Over time, mistakes in a strategy will be uncovered. Getting caught up in a market’s mood instead of adhering to a strategy, can cause long term complications for an investor, especially in extreme market conditions.

2007 stands out as a great example of extreme market conditions that uncovered poor underwriting standards. Prior to 2007, stable rent appreciation made overly-optimistic underwriting strategies seem appropriate. Poor underwriting was rewarded, and thus, many companies compromised their strategies by chasing deals based upon past rent appreciation. These compromised standards built to a crescendo by 2007, and by the time of the Global Financial Crisis, many of the speculative deals bought prior to 2008 suffered. Tishman Speyer’s 2006 deal for the Stuyvesant Town/Peter Cooper Village complex in New York City is a great example of a firm compromising underwriting standards. The firm vastly over-payed for the property in New York City, and subsequently lost their investors’ money. This was one of the largest commercial real estate blunders during the Global Financial Crisis, and is a good example of how even the best firms can get caught in the froth of a market.

Although it seems easy to realize these forecasting errors in hindsight, the main lesson that can be derived from the downturn, and deals like Stuyvesant Town/Peter Cooper Village, is just how hard it is to time the market. Much has been written on the subject of market timing, but industry veterans who have navigated recessions will tell you to never force a deal, and to never compromise your underwriting standards to get a deal done. Over time, compromising one’s standards will inevitably come back home to roost. Finding value in the buy has been the hallmark of many great careers, and with a patient and disciplined value approach, one can improve their odds of being a good investor. So, how do the value-added investors do it?

Finding A Property

Finding a property takes time and patience. Many good investors will do less than one deal for every hundred they consider. A large volume of the deals that make it to the market are too expensive to repair or do not offer solid risk-adjusted returns. Sometimes the product is functionally obsolete, or requires major structural changes to make it viable again. Other times the local market simply will not support the rent growth necessary to hit targeted returns.

Structural issues which may be uncovered during ownership can cause cost overruns during construction. Knowing these issues upfront is important when underwriting a deal. With proper due diligence, these problems may be avoided at the outset. When an investor has a property under option, they will have the property inspected. It is up to the investor to choose a trustworthy inspector with good credentials to uncover any structural problems.

An acquisition decision can set a project up for success or failure before construction or repositioning even begins. Finding a property at a discount is the surest way to justify rent growth for your property during a reposition of the asset. Finding the discount is less straightforward. If a property goes to auction, it can be like a game of high-stakes poker, with a twist. The winner doesn’t always win, which is why it is essential to have a number, and stick to it.

While most firms understand this, they vary greatly in their acquisition strategies. In general, an investor will begin their hunt by looking for undervalued and underperforming assets in areas with which they are already familiar. Many concentrate on a specific geographical area or region where they know the right brokers and have expertise about what drives the local economies. Targeting a geographic area close to home also makes it easier to deal with problems on the property.

Once the geographical focus has been established, firms will begin to look for an acquisition target. In most areas, the investor will have different options with regard to the type of multifamily building he or she wishes to own. In most large and mid-size markets, investors will find a tremendous amount of diverse opportunities within the multifamily sector, which is one of the reasons why it is such an intriguing asset class.

This range of acquisition targets, which vary in age, size, quality, and location, allow investors to specialize. A fund will normally focus on a certain type of asset, or look for properties in a certain value range. While opportunities come in all shapes and sizes, the common thread for a value investor is that a targeted investment will underperform its peers, thus providing a value opportunity to pursue.

To consistently find value, firms need to cultivate relationships with brokers in the target area, and seek to understand the sources of attractive value opportunities. Brokers are often the gatekeepers of early information about sales, especially “pocket listings,” whereby a broker will shop a deal to exclusive buyers whom the broker knows can afford the property and close quickly. Pocket or “off-market” listings that do not make it to the open market are oftentimes priced below the value they would fetch at a well-publicized auction, or market value. This is especially true in multifamily, which has a larger participating buyer pool, resulting in greater liquidity than the other major property types, and subsequently, compressed capitalization rates.

For a pocket or off-market listing, brokers will typically go to a buyer with whom they have a longstanding relationship. If a firm is entering a new market, it pays to establish and cultivate relationships with brokers. One way firms do this is by offering ancillary incentives to brokers, such as co-investment opportunities. Nurturing these relationships is very important when looking for value, and can be the difference between acquiring an exclusive off-market listing, or watching another investor make the acquisition you would have made at a price you would have paid.

Another way to find value is through a third-party manager. A third-party manager with deep roots in an area can act as “boots on the ground” for new opportunities. This is one reason why investors often utilize the services of an institutional-quality manager that is strictly a management company and not an owner/operator. A company which is both an owner and an operator may have the capital to acquire a property that you’d like to pursue, thus becoming a competitor. On the other hand, an operator which is strictly a management company will be incentivized to bring that same property to a current client for the expectation of future management fees.

After a firm has found a property with sufficient value, it must make an offer as quickly as possible, but with close attention to every detail throughout the acquisition process. The firm will always undertake some sort of due diligence prior to making the offer, and will usually have an option period to carry out additional due diligence. That said, if the deal is a pocket listing and the price is below market value, the majority of the research will come during the option period in order to make an expedient offer.

Making a Decision

During the option period, an investor will conduct an in-depth market analysis as well as a property inspection to aid in their property underwriting. Ultimately, the investor’s decision to purchase the property will hinge on whether or not they believe the property will exceed their targeted return. Proper due diligence at this stage is critical to the eventual underwriting of the property, as an investor will begin to have an idea about what returns the asset can generate and how it should be underwritten.

During the underwriting process, many different factors will be analyzed, such as the local economy, demographics, and other quantifiable factors. Factors that can influence both the demand for and supply of housing in the area are of particular interest. These factors include export-based economic indicators, such as location quotients from the Bureau of Labor Statistics, as well as analyses which consider elements such as nearby jobs and wages.

Investors need to minimize their risk and one of the biggest problems when looking at or acquiring the property is the possibility of overlooking something important. These oversights can come in the form of market risk, where one may overlook factors that affect supply and demand in the market, or at the property level, where unexpected occurrences can affect profits and decrease returns. The distance the property is from the investor can exacerbate an owner’s ability to deal with these types of problems.

Investors will look at indicators that can describe the economic drivers in the market, and give them a snapshot of the underlying economic conditions affecting the property’s performance. The market analysis, either performed in-house or by a consultant, will lead the investment team to any assumptions necessary for underwriting a deal. These assumptions help the investor determine if they can grow rents and exit the property at a value which exceeds their targeted returns.

One point to note is that a regulatory process analysis is not a high priority when dealing with a multifamily value-add proposition, unless there are rent regulations or restrictive housing policies in the local market. This is because there is usually no zoning change required, as there will be no change of use. In addition, if no restrictive local housing regulations exist, then State and Federal regulations may take precedent. In general, regulations at the State and Federal levels are already well-understood by investors of a particular property type, and especially so for multifamily. This lack of regulatory risk helps the investment reach favorable risk-adjusted returns, one of the most attractive features of the value-added strategy.

An investor will also complete a property inspection in addition to a market analysis. When judging potential acquisitions, an investor would prefer to find properties in need of repair which are not functionally obsolete. Sometimes an investor will forego a deal because of structural problems uncovered during an inspection. Other times an investor will find that the amount of work that needs to be done is related to either aesthetic or managerial problems. Properties that needs minor structural changes on a per-unit basis are often solid acquisition targets because they can provide a high-yield opportunity for less risk.

An investor will hire a site inspector whose job it is to figure out the physical condition of the property. The inspector’s report will provide details about potential problems on the property and will uncover any major issues including but not limited to: asbestos, lead paint, foundation issues, and any major building code violations. In addition to the inspection report, an investor will also commit a walk-through of the site. Generally, this will include a team of people including the investor, inspector, the site manager, and the construction manager. The team will walk the property, scoping out every unit, and providing feedback which will be outlined in a detailed assessment. This assessment will set the stage for both the underwriting of the property and the detailed turnaround strategy necessary to realize value in the property. Below is a general overview of certain changes an investor might expect to make to any given property.

Cosmetic/Aesthetic: Cosmetic changes increase a property’s value by increasing its appeal to both current and potential residents. These activities include painting, improved or added signage, landscaping, restriping and resurfacing parking lots, updating both interior and exterior finishes, updating the website, and even changing the name of the complex. This is the least-involved strategy of the three, but aesthetic changes can have a significant impact on both vacancy and rental rates.

Some of these changes might seem simple, but can actually have a substantial impact on property performance. One example would be changing the name to include the city or town of the local area to increase the number of hits on a search engine, which is generally the first place prospective tenants look when searching for a new apartment.

Structural & Major Renovations: Renovations involving structural or major changes to the property generally require the most involvement. These types of renovations can include but are not limited to: roof replacement, foundation repair, converting utility metering to a per-unit basis, changing mechanical systems, altering floor plans, updating bathrooms and kitchen, replacing outdated flooring, and constructing or renovating common area amenities. Some examples of different amenities could include clubhouses, pools, outdoor grills and kitchens, exercise facilities, tennis courts, and gaming rooms. Because this type of renovation is the most involved, it is often the most capital intensive, but it can also represent the best return on investment. In-room amenity upgrades are generally recognized as yielding the highest return on investment.

Operational: Value can often be gained or lost by changing the way a property operates. Investors typically add value here by changing managers or management companies. A solid management strategy is key to unlocking value, and this can be done a few different ways. Managers may do this by not renewing the leases of disuptive tenants, marking rents to market, collecting overdue rents, and adding additional revenue sources like laundry and paid parking. In general, an underperforming property will often contain value that can be captured by a managerial upgrade. These operational issues will be dealt with on a case by case basis, and are extremely important for the property to function efficiently.

Financing

The first order of business when acquiring a property is securing the financing. A multifamily investment is usually financed using a mix of debt and equity. Debt is usually acquired from the bank based upon the value of the property. A bank will typically loan out approximately 80% of the value of a multifamily property. Multifamily is generally considered one of the easiest asset classes to finance due to the abundance loans backed by government-sponsored enterprises such as Fannie Mae and Freddie Mac. These agencies underwrite multifamily as a stable investment platform and are therefore willing to back loans based on up to 80% (or more) of the property value. The amount of money one can get based on the property’s value is a metric known as the loan-to-value ratio, or LTV.

Though an investor will acquire their loan from the bank based upon the loan to value ratio, they will underwrite the deal based upon the loan to cost ratio, or LTC. An investor will generally look at the loan on a total cost basis, including the expenses accrued while implementing their value-add strategy. Investors use the LTC metric because it measures the percentage of debt that they can put towards the total cost of the project, including the purchase and renovation of the property. This allows the buyer to underwrite the entire project.

Loan to Cost and Loan to Value are both related. As a rule of thumb, an investor will be able to get a loan for 80% of the purchase price, while this same amount may cover around 60-70% of the total cost of the project. While many properties differ, there are many cases in which garden-style class B-C apartments with this LTC ratio can realize an 8% yield out of the gate, assuming current market capitalization rates for multifamily trades. Investors will then augment the property via an improvement strategy, and boost their returns to the 15-20% range on a cost-return basis. This 15-20% range is what makes the property a good investment, and allows a fund to attract other equity sources to the investment.

Investment Strategy

Management

Once the project is financed, and the investor closes on the property, it is time to start implementing the improvement strategy. There will be a number of things to do, but putting new management in place is often priority number one. An institutional-quality manager will create efficiencies, and will be more motivated to take on the responsibilities of managing the property during its repositioning. Good managers communicate effectively, which creates a sense of community in the apartment complex, decreasing the number of maintenance issues, and making the asset more inviting to potential customers.

Properties that have been mismanaged, or lack a sense of community pride will often have tenants who have become apathetic in their payments or maintenance requests. In these situations, the third-party manager will be responsible for resolving tenant concerns on a more active basis. As renovations occur, rents will rise, and tenants will turn over. It is up to the third-party manager to attract new tenants to the property, and expand the renter pool that the property may access through its marketing.

Once an investor has a third-party manager in place, it is time to begin working with the management company’s construction arm (or outside project manager) to devise an improvement plan. There are many different ways to go about implementing an improvement strategy, but a general rule of thumb for the allocation of improvements is 30% to the exterior and 70% to the interior. The third-party manager ideally will have had experience working with investors in the past, and should be receptive to their needs. Institutional-quality managers often have experienced construction management teams who will be able to work with the investor and handle all of the necessary upgrades to the property.

The construction management team will typically include a capital projects manager whose job it is to oversee the improvement strategy. The investor might pay the capital projects manager a 6% fee for all of the projects that they manage on site. With experience in a particular geographical location, the project manager will bring important contractor relationships to the project. The importance of relationships with general and sub-contractors should not be understated, as stable, repeat business represents some of the greatest incentives for firms in the construction industry. A capital projects manager with long-term relationships and a long-term business outlook can negotiate the best pricing.

Once the capital projects manager is on board, the investor will begin to work with the team to devise an improvement strategy for the property. Generally, an owner will walk through the property with the project manager to come up with ideas for improvement, and to set a renovation schedule. Establishing a schedule is an important part of the improvement strategy, as it allows the investor and the capital project manager to collaborate on a timeline and measure progress.

Construction

After the investor and a third-party manager have set a schedule, they will begin the planned renovations as part of the value-added strategy. Generally, an investor will start with anything that includes emergency repairs, or aspects of the project that increase the curb appeal of the property. Remediating structural problems and increasing curb appeal will have a positive impact on property value, and will attract new residents willing to pay higher rents. Cosmetic upgrades include smaller items like new coats of paint, asphalt overlays, and landscaping.

In addition to cosmetic repairs, an investor will also consider adding amenities to be completed during the appropriate time in the leasing cycle. Upgraded facilities such as pools, clubhouses, fitness centers, game rooms, and tennis courts may attract new residents to the property, and make use of underutilized space. Residents like to have options, especially when it comes to activities and entertainment. More importantly, given a strong market, they are willing to pay extra for those entertainment options. Upgrading a property’s amenity package can influence which residential market the property competes in, and the type of renter it attracts.

In addition to cosmetic repairs and amenity upgrades, interior updates may be required. Interior refurbishments usually account for 70% of the improvement costs, and generally take one to two years to complete. This is due to the fact that interior renovations must be scheduled around tenants, and are normally only achieved once a unit is vacated for an appropriate period of time. Turnover will happen naturally as management begins to increase rents. The third-party manager will be able to give investors a rough idea of the turnover schedule before the process begins.

This schedule is important as investors usually prefer to refurbish units as they turnover rather than all at once. This is because investors can use accrued free cash flow to pay for all or part of the construction expenditures. Paying for renovation costs out of cash flow can increase the overall return for the investor, and benefit the property’s leasing operations by turning over units. In most value-added opportunities, new tenants will sign leases on a different schedule than existing tenants as the interiors of existing rooms are renovated.

These renovations can include new cabinet fronts, hardware, carpets, vinyl wood flooring, lighting packages to spruce up in dimly-lit rooms, new stainless steel appliances, and updated bathroom vanities. Upgrading units is at the core of any strategy, as it leads to the highest returns for every dollar put into the property. In general, the investor should be targeting roughly a 25-30% return on investment for cosmetic interior renovations.

Once construction is completed and all of the cosmetics, amenities, and interiors have been updated, the property should enjoy an increase in value. In theory, this will dovetail with the leasing strategy, and attract higher-paying tenants throughout the property. As income grows, the value of the property will grow, and the investor will need to make a decision whether to hold the asset, or exit the property.

The Exit

There are a variety of factors that can affect the timing of the exit, including the capital market, local market conditions, and the fund’s targeted returns. In addition, each property will be subject to an individual owner’s interests, which may change the targeted exit conditions. A general overview of favorable exit conditions follows:

Fund Strategy

It is often in the best interest of a fund to realize a liquidity event sooner rather than later. The sooner the owner sells the property after maximizing NOI, the quicker they will reclaim their capital, including preferred returns. In addition, decreasing hold time will boost the internal rate of return, which will generally have implications for the percentage of profits that general partners (GPs) receive through the use of IRR-based promote hurdles.

Normally, preferred returns are tied to IRR, a measure of the net cash flow and time value of money. A quicker sale will boost IRR and increase returns for a general partner and their investors. Nearly 80% of the upside of a deal for the GP is often contained in the promote, so the sooner a GP can realize a liquidity event (a sale of the property), the sooner they will realize the majority of their upside.

That said, not all funds are structured for a quick investment exit. The current market, which is starved for yield, sees multifamily as a stable cash flow investment, lending itself to longer holding periods. Some firms pursuing yield can realize a 12-15% IRR for holding periods of 7-10 years, though this is completely dependent on the strategy and management of the assets in the portfolio. These types of funds can be preferable to investors who are targeting yield and will prefer a continued investment that offers sustained cash-on-cash returns. Even so, when the GP feels that the potential market price of the property has exceeded its value by a significant degree, they might be incentivized to sell. In such cases, even longer-term yield-oriented funds may exit early to provide their investors with a superior return. Properties experiencing extreme rent growth will fall into this category. Investors could also consider an early exit if they believe they are approaching a peak in the market cycle.

The ultimate goal of a value-added investment strategy is to exit the property and add value for investors. A fund will have the discretion to sell if they believe an exit is in the best interest of their investors. Should a fund exit a property and exceed their targeted IRR, then they will have met their goal by implementing a strategy that ultimately meets and exceeds their assurance to investors.

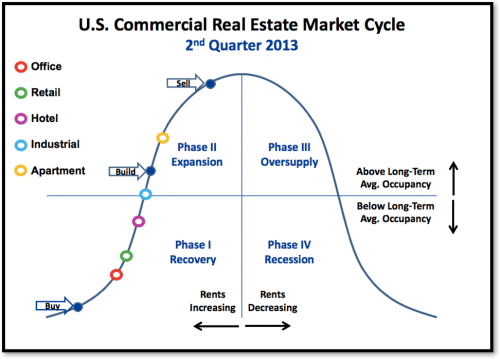

Local Market Conditions

Local market conditions also affect the exit, and are a powerful force when it comes to property value. Market conditions run in cycles and are directly tied to the interaction between the underlying economy in an area, which creates demand, and the supply of available units. Books have been written on the workings of the market cycle and there are many different strategies available when it comes to judging the market. Certain strategies will allow an investor to minimize risk, such as applying more conservative leverage to a project by entering into a 10-year loan and paying down principal, or going with a fixed rate mortgage. As an investor, tools such as using conservative leverage will help to support a risk-adjusted strategy, however it is up to each individual to find the right time to sell. After the firm sells the property and exits, they will have completed the value-added process.

Conclusion

Successful execution of a multifamily investment offers excellent risk-adjusted returns when compared to other classes of real estate. When augmented by a value-added strategy, the stable long-term cash flows typical in multifamily investments can be amplified to secure more attractive risk-adjusted returns by buying properties that have identifiable and fixable problems. The success of this strategy depends on the knowledge and execution of the ownership and management team, which is why it is essential to assess each opportunity from the perspective of risk, reward, and capability.