India’s economy is poised to leapfrog from its current seventh-place position to the third-largest economy in the world by 2027 with US$6 trillion gross domestic product according to a recent Morgan Stanley research paper. India’s e-commerce market has reached US$33 billion registering a 19.1 percent growth rate in 2016-2017, as per the recently-published Economic Survey 2018 by the Indian government. The e-commerce market is expected to reach US$64 billion by 2020 and US$200 billion by 2026 from US$38.5 billion as of 2017. Logistics is a major driver of the e-commerce retail industry and is an important point of differentiation between market players aiming at better customer satisfaction and service.

What does this mean for international real estate investors? Industrial real estate is quickly emerging as the go-to asset class for investors and developers, as India’s consumption and e-commerce story gets a boost from the government’s “Make in India” initiative and the goods and services tax (GST). The total warehousing space requirement is expected to grow at a CAGR of 8 percent from 621 million square feet in 2016 to 839 million square feet by 2020 as per Knight Frank India.

There has already been interest demonstrated by the international investment community towards Indian logistics. One of the early entrants into the logistics market in India was Realterm Logistics, a leading North American industrial real estate investment firm that owns interests in and manages over 300 operating and development properties. The company partnered with a local private equity fund, Everstone Capital, to form IndoSpace in 2007. In May 2017, the Canada Pension Plan Investment Board (CPPIB) and IndoSpace announced the creation of IndoSpace Core, a joint venture that will focus on acquiring and developing modern logistics facilities in India worth US$1.3 billion. IndoSpace Core has committed to acquire 13 well-located industrial and logistics parks totaling approximately 14 million square feet from current IndoSpace development funds. The assets are prime industrial properties located in the top industrial and logistics hubs in India, including Chennai, Pune, Mumbai, Delhi, and Bangalore.

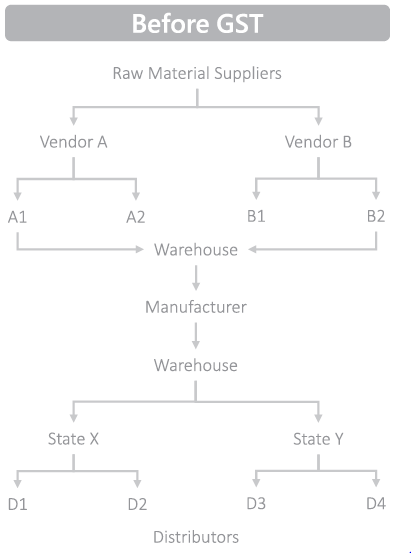

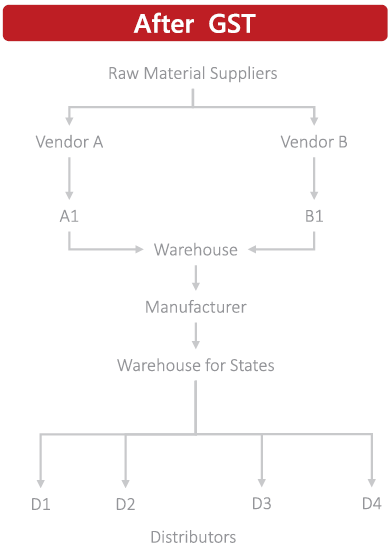

GST implementation drives the growth of regional distribution centers

The GST implementation will help streamline the flow of goods between states and create the need for regional distribution centers. Below is a graph that shows the difference in movement of goods, pre- and post-GST.

Pre-GST logistics players in India had been maintaining multiple warehouses across states to avoid Central and state entry taxes. Most of these warehouses were operating below their capacity and thus adding to their operational inefficiencies. Post-GST India will become one single market wherein goods can move freely inter-state without any levy. As per property advisory Knight Frank’s India Warehousing Report 2018, the National Capital Region attracted the highest leasing transactions in the warehousing space at 6.5 million square feet in 2017, followed by Mumbai at 5.2 million square feet. Leasing deals in the warehousing sector across key Indian markets rose to 25.7 million square feet in 2017, up 85 percent from the previous year. Post-GST, there has been a spike in demand by almost 100 percent as companies who were until now in a wait-and-see mode have now moved into execution mode. For the first time, we are witnessing consolidation and expansion of warehousing space. This increase in demand from sectors like e-commerce, 3PLs, consumer durables, FMCG and manufacturing coupled with a requirement for larger warehouses has opened up the field for more and more organized players.

FDI into e-commerce pushes the need for warehouses

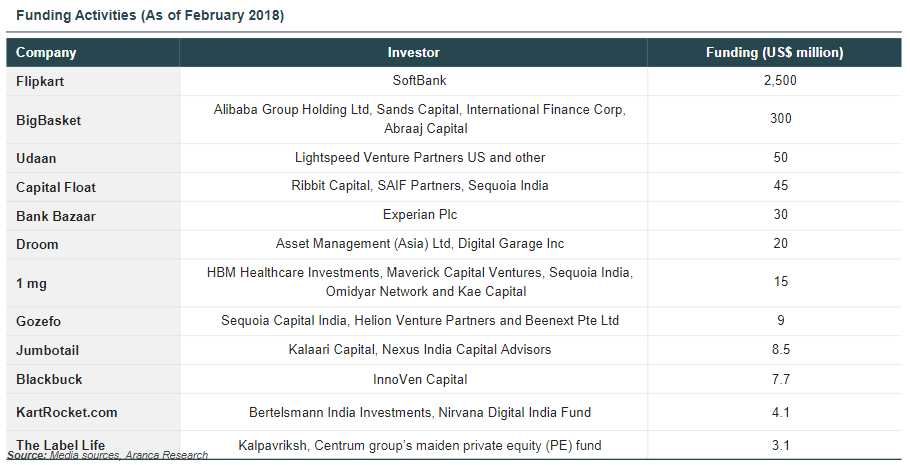

The new Foreign Direct Investment (FDI) policy rules and regulations for India in the e-commerce market have permitted 100 percent FDI in the e-commerce marketplace model under the automatic route. The first half of 2017 recorded 26 startup funding deals of value US$100 million and above, aggregating to US$7.7 billion and accounting for 68 percent of investments during the period.

Focus on the investments in warehousing

The prime beneficiaries of the new wave of growth in warehousing will be the peripheral locations of tier 1 and tier 2 cities. This investment comes at the back of the fact that nearly US$2 billion was invested in 2017. Of all the categories, warehousing will be witnessing the highest investment of over US$5 billion in the next 3 years, mostly in creating storage facilities for retail and consumer goods. The cold storage and agricultural warehousing would see about approximately US$1 billion in investment. Container storage would be attracting approximately US$100 million in the same period mostly to boost India’s logistical prowess. Overall growth in e-commerce and a shortening turnaround time for delivery has necessitated a sharp growth in warehousing in the country.

Some other key transactions in India

Global logistics developer e-Shang Redwood (ESR) plans to secure almost 600 acres of land across various locations in India to set up industrial and logistics parks and expects to launch its first project by the fourth quarter of 2018. ESR aims to invest around US$100 million annually and is looking to either buy or form joint ventures for land parcels of 50-150 acres each with landowners or developers. ESR plans to be one of the largest industrial and logistics developers in India by 2022. In the first phase, it will look at tier I cities like Mumbai, Pune, Chennai, Bengaluru, Hyderabad and National Capital Region (NCR) where there is a clear gap between demand and high-quality supply.

Apart from Canada’s Brookfield Asset Management Inc. which is planning to enter the industrial real estate space, Sydney’s LOGOS Group and Assetz Property Group from Singapore partnered in 2017 and are scouting for land. Embassy Industrial Parks Pvt. Ltd, Ascendas-Singbridge Group, and Mahindra Lifespace Developers Ltd also plan to build industrial parks and clusters.

Key concerns

Investors need to be careful about their aggressive plans. A large portion of the new warehouse inventory is speculative. We will have to see how the new product is absorbed and also how quickly. Currency fluctuation risk also still looms large. An April 2018 report from Kotak Economic Research shows that India’s current account deficit in the current fiscal year is forecast to be the highest in six years. The report projects three scenarios, with Brent crude prices at an average of US$65, US$70 and US$75 per barrel. Even under the US$65 per barrel scenario, the current account deficit is likely to be 2.4 percent of GDP, higher than in 2013-14. Finally, with a lot of pension funds investing in development deals instead of investing in stabilized properties, the exit options are yet unclear. Nonetheless, investor interest in Indian warehousing continues to increase as the global search for yield continues.

[1] IMPACT OF GST ON LOGISTICS INDUSTRY, 2017 – https://cleartax.in/s/impact-gst-logistics-industry