As we enter 2019, housing affordability continues to plague much of the United States with no sign of relenting. The end of 2018 witnessed a sputtering economy with home values leveling off, only to continue their upward trajectory in the month of January, and into the foreseeable future. Meanwhile, a dire lack of inventory will define the coming decade, and 2019 is expected to witness as much as a 2% drop in home sales (Dollinger, 2018). This is especially problematic for new homebuyers entering the marketplace, as developers have until only recently focused on luxury options (Berens, 2019), leaving fewer and fewer affordable choices. New data from the US Census Bureau projects that 325,000 new rental units must come online every year until 2030 to meet new housing demand.

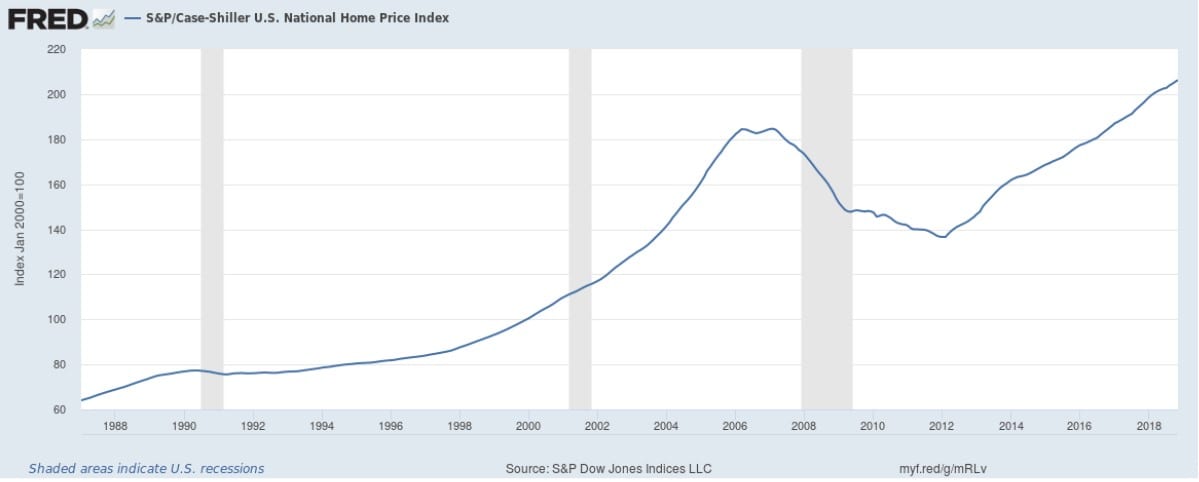

At the same time as affordable housing is in critical demand, older demographics continue to enjoy high levels of homeownership. Even low/no-income Americans in the 65+ age group often find themselves “house-rich, cash-poor” with assets to their name but little liquidity for everyday expenditures, such as utilities, groceries, and essential healthcare. As much as 65% of Americans aged 65+ live in large single-family homes with free-and-clear titles, and those with some level of mortgage debt still had median equity in their homes of nearly $110,000 as home values bottomed out in 2012 (Butrica & Mudrazija, 2016). Since 2012, home prices have matched their pre-recession trajectory, rising in value by over 50%, and the population over age 65 has grown by over 7 million (U.S. Census Bureau, 2018).

One viable solution for seniors to age in place, and to free up inventory for new homebuyers, is through a “sale-care-redevelop” process. This is an attractive option for seniors with no children or immediate family and who wish to age with dignity in their own home, as opposed to more common “reverse mortgages”, which offer usurious rates.

As of 2018, Americans with mortgages hold more than $6 trillion in liquefiable home equity, which is nearly 3 times as much as at the bottom of the recession in 2012 (Black Knight, 2018). In recent years, companies have attempted to tap into this value through resurgent investment vehicles. Unison is one such company, though not specifically targeted at seniors, which is offering “ownership shares” of single-family homes in exchange for cash. The company, through its HomeOwner program, will pay out up to 20% of a home’s value and collect no interest or principal payments until the homeowner sells. At the time of the sale, Unison collects its original principal plus a share – averaging 35% – of the home’s appreciated value from the time of the contract. In an example quoted from its website, a 10% share paid to a homeowner in the year 2000, for a home purchased for $1,000,000 in 1987, would be worth $557,000 to Unison at prevailing home values in 2017, and over $2 million to the homeowner.

Aside from offerings like Unison’s, the more common solution for this demographic group looking to supplement their incomes has been through reverse mortgages, which sell incremental home equity to a lender in exchange for a fixed monthly payment. These arrangements often offer unfavorable dividends which are insufficient to cover everyday expenses, and the fees and interest can significantly detract from the total amount of equity available. As an alternative, private companies can obtain ownership of the property, pay a fractional lump sum to the owner, and provide home care and property maintenance services for the tenure of the seller’s life. In exchange, the new owners obtain options for future redevelopment. This arrangement is particularly beneficial for childless seniors who have no plans for their real estate and no access to care through their family network.

At the close of the “care” term, developers can take advantage of the large home size typified by this demographic. In today’s tight rental market, planners have begun to look favorably on expanding the density allowance in single family neighborhoods. Developers may find success applying for variances for accessory dwelling units, and harvest returns when they resell the properties.

| Pros for Senior Homeowners | Pros for Landlords |

|

– Age in place – Have liquidity to pay their bills – Enjoy some level of home care – Property maintenance – No estate planning, no probate issues

|

– Capital preservation – IRR’s driven by renovation, resale, and paydown of debt where applicable – Growing pipeline of prospective properties as US population continues to age |

In 2012, 22% of Americans aged 65 or older had no children and owned homes (Storrs, 2015). Among these owner-occupier seniors, the median amount of home equity was $129,000, with a median home value of $155,000. According to the same study, 58.5% of seniors in the bottom third of the income segmentation owned homes, and the median value of their equity was $77,000 (Kaul & Goodman, 2017). In absolute terms, this amounts to over $450 billion in home equity available to 6.1 million low-income seniors with potential care and succession issues as they age (U.S. Census Bureau, 2017). Clearly there is a large pool of value waiting to be unlocked, and it could be, at least in part, the answer to unlocking a treasure trove of inventory.

. . .

Works Cited:

Berens, M. (2019, January 2). Housing pressures cool luxury home market. Multi-Briefs.

Black Knight. (2018). July Mortgage Monitor. Jacksonville, FL: Black Knight Financial Solutions.

Butrica, B., & Mudrazija, S. (2016, October). Home Equity Patterns among Older American Households . Urban Institute.

Dollinger, J. (2018, November 2). 2019 Forecast: Existing-Home Sales to Stabilize and Price Growth to Continue. National Association of Realtors.

Kaul, K., & Goodman, L. (2017). Seniors’ Access to Home Equity: Identifying Existing Mechanisms and Impediments to Broader Adoption . Washington, DC: Urban Institute.

Storrs, C. (2015, May 18). The ‘elder orphans’ of the Baby Boom generation. CNN.

U.S. Census Bureau. (2017). Facts for Features: Older Americans Month: May 2017. Washington, DC: U.S. Census Bureau.

U.S. Census Bureau. (2018). American Fact Finder. Washington, DC: US Census Bureau.