One of the most followed real estate sagas of 2016 was the case of New York REIT (NYRT), in which shareholders actively and publicly faced off against NYRT management in their opposition to an agreed-upon merger with Washington, D.C.-based JBG Companies (JBG). The NYRT-JBG story highlights several modern day issues for REITs.

First, it illustrates the heightened expectations of investors when a REIT focuses on primary or “gateway” markets vs. non-primary markets. In this instance, the performance of the DC office market has lagged that of New York over the past few years. One main point of investors’ opposition to the merger was the fact that many bought NYRT because it was marketed as a pure play on Manhattan real estate, which the merger would have diluted via adding a portfolio of DC-area assets. This dynamic is also evident in the fact that Vornado Realty Trust has publicly stated its intention to sell its DC assets in order to concentrate on its core New York City properties.

Second, the NYRT case highlights the widespread perception that externally-managed REITs are inherently less able to align shareholders’ interests with those of management. Activist investors played a prominent role in this story, and their aggressive push for change at NYRT should be seen as a sign of things to come. Indeed, as real estate and REITs gain further acceptance as a primary asset class, the scenario will likely be seen more often in the future as more activist investors enter the space. In this case, the hedge fund WW Investors and activist investor Jonathan Litt were the most public opponents of NYRT management. The dissident investors advocated plans that included extricating NYRT from its external-advisor structure in addition to the sale of certain assets at market prices.

On May 25, 2016, NYRT and JBG announced their plan to combine into a publicly-traded $8.4 billion enterprise value REIT, to be called JBG Realty Trust. Executives of both firms touted the benefits of diversification, with a portfolio that would be concentrated in the DC and New York City markets. The announcement brought to a close a strategic review that had been initiated by NYRT in late 2015 to explore options to unlock value for shareholders, including a sale of the firm. The negative reaction to the announcement was swift, with NYRT stock dropping 8% the following day. Activist shareholders Michael Ashner and Steven Witkoff, joint owners of WW Investors LLC, stated that the JBG deal was “one of the worst strategic transactions proposed to stockholders by a REIT board in recent memory.” Ashner and Witkoff initiated a proxy battle after the merger announcement, nominating five of their own candidates to replace the sitting NYRT board.

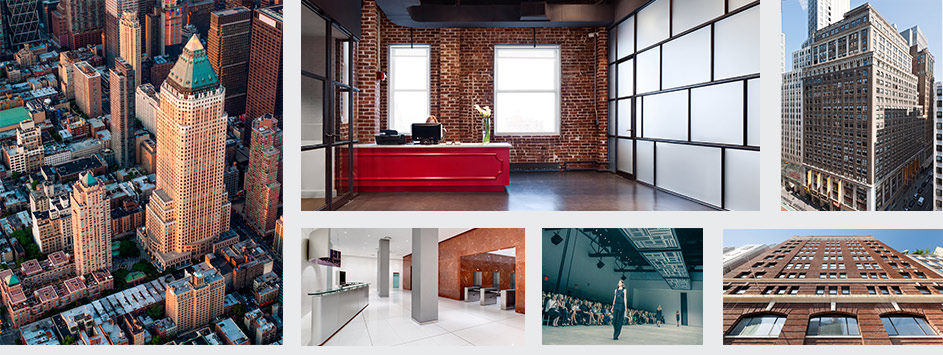

This image, taken from NYRT marketing materials, illustrates its pitch of being a pure-play on New York City real estate

The reaction summed up what had been a frustrating two years for NYRT shareholders. Prior to its April 2014 IPO, NYRT was touted as the only REIT solely focused on New York City real estate, with 97% of its assets in Manhattan and 100% of its portfolio located in the city. At the time, New York REIT’s portfolio consisted of nine office properties, eight retail properties, one hotel and one parking structure. The flagship property, Worldwide Plaza, is a 1.8 million square-foot skyscraper on Eighth Avenue that contains the North American headquarters of Nomura Holdings Inc. and the corporate law firm Cravath, Swaine & Moore LLP. Other notable properties include 1440 Broadway, a 750,000-square-foot tower at Broadway and 41st Street near Times Square, and the Twitter Building in Chelsea, of which the social media firm is the largest tenant.

An overview of selected NYRT assets, including One Worldwide Plaza (left), The Twitter Building (center) and 1440 Broadway (right)

NYRT shares never gained traction after the IPO, dropping below $10 and hovering around $9-10 for much of 2015. As mentioned, one of the key factors driving the chronic undervaluation of NYRT was an external management arrangement with a firm headed by former NYRT executive Nicholas Schorsch. The potential conflicts of interest centered around compensation to the advisor as well as the existence of an outsize termination fee. To make matters worse, Schorsch had resigned in disgrace from the board of New York REIT and 12 other companies in late 2014 following the disclosure of accounting inaccuracies at one of his companies, American Realty Capital. To illustrate, a “change in control” at NYRT, such as a merger, would have triggered long-term performance incentives that would benefit the external manager, according to WW Investors. WW Investors estimated that the termination fee would be equal to a “significant” portion of NYRT’s market capitalization, an arrangement that investors would naturally be opposed to.

In the months after the IPO, activist investors such as WW Investors and Land and Buildings’ Jonathan Litt entered the fray, urging NYRT management to liquidate the REIT. With the pressure building, NYRT announced in October 2015 that it had hired Eastdil Secured to “vet an entity-level sale of the company.” While the six-month strategic review process led to the generation of more than 80 nondisclosure agreements with potential buyers, NYRT management ultimately did not act on any offers.

On May 2 of this year, New York REIT was rumored to be in talks with JBG as well as SL Green Realty Corp, another publicly-traded REIT that is known for owning more commercial square footage in Manhattan than any other firm. Despite the potential synergies, SL Green denied the rumor, according to Bloomberg News.

According to WW Investors, the May 25 announcement came two weeks after an “attractive” proposal was made following the early May rumors. In its first quarter earnings release on May 10, NYRT management stated that its strategic review process was “ongoing,” but it declined to host a conference call, as would otherwise have been the standard practice. WW Investors immediately took the REIT to task for not responding to the proposal, making the alleged proposal public in a May 11 letter. Ashner wrote that “in my twenty years of personal involvement in public companies, I cannot recall such an egregious disregard of process, nay simple courtesy,” noting that NYRT had asked for time to conduct its strategic review. “Yet, when given the opportunity to further the process, the company and its advisors demonstrate both a clear disdain of duty and ugly discourtesy to potential suitors.”

Under the proposed deal with JBG, New York REIT stockholders would have owned roughly 34.8% of the combined company, with JBG stockholders holding the other 65.2%. Approximately 78% of the portfolio (by rentable SF) would have been located in the DC region, with the balance in New York City.

After a difficult two months, on August 2 NYRT and JBG announced that they had mutually agreed to terminate their merger deal. NYRT paid JBG a $9.5 million termination fee, and released a statement stating that “while both parties in this transaction believed that the NYRT-JBG combination represented a clear path to maximizing long-term value for NYRT stockholders, investors were clear in their preference for a liquidation to generate near-term cash.” According to Bloomberg, it had “become clear shareholders didn’t support the deal and that any modification of the deal was unlikely to gain shareholder approval, so it made sense to terminate the deal rather than proceed with a formal shareholder vote.”

NYRT’s stock price jumped in response to the news, rising 5.8% over the next two trading days. Its August 3 closing of $10.03 was 6.3% below the company’s opening price on April 15, 2014, its first day of trading on the NYSE. By contrast, during that same time frame the SNL U.S. REIT Equity index rose by 26.8%.

As New York REIT moves to sell off its properties, an SNL Real Estate analysis finds the company’s portfolio carries an estimated value of $1.74 billion, with individual properties ranging in value from $5.4 million to $648.0 million. On September 7, NYRT announced that it would initiate a search for a new external manager, and as of this writing that process is ongoing.